If you only looked at shipment data, you could easily conclude that the freight market is still soft.

If you only looked at pricing data, you might conclude that the market is tightening rapidly.

The reality is somewhere in between. That is what makes the current freight environment so challenging, and so important to understand.

The latest freight market update shows a market where shipment demand remains uneven across industries, yet capacity is tightening faster than many expected. As a result, truckload rates are climbing, carrier availability is becoming more selective, and mode decisions are becoming more important for both brokers and shippers.

For experienced brokers, this environment creates opportunity. For shippers, it creates risk if transportation strategies remain based on assumptions from the past two years.

The more useful question now isn’t whether freight demand is strong or weak. It’s whether available capacity is keeping pace with the freight that needs to move.

The Freight-Market Paradox in 2026

One of the biggest misconceptions in today’s freight market update is that shipment growth and pricing growth must happen simultaneously.

Historically, freight markets followed a relatively predictable pattern. Demand increased, capacity tightened, and rates followed. Demand declined, excess capacity entered the market, and pricing softened.

The current market is behaving differently.

While freight activity remains inconsistent across sectors, capacity has continued to exit the marketplace. Many carriers that struggled through the prolonged downturn reduced equipment purchases, delayed expansion plans, consolidated operations, or exited entirely. That reduction in available capacity is beginning to influence pricing even before a broad freight recovery has fully materialized.

This creates a market paradox:

| Indicator | Current Trend |

| Shipment Demand | Uneven |

| Available Capacity | Tightening |

| Spot Market Activity | Improving |

| Carrier Quality Standards | Increasing |

| Truckload Rates | Rising |

| Intermodal Freight Activity | Growing |

What makes this environment unique is that supply-side changes are having a greater impact than demand-side growth.

In practical terms, a shipper doesn’t need freight volumes to increase dramatically for transportation costs to rise. If fewer qualified trucks are available, competition for those trucks increases regardless of whether shipment growth remains modest.

For brokers, this means traditional market narratives may no longer be sufficient when communicating with customers. Simply saying “the market is soft” ignores the growing pressure on capacity and pricing.

Experienced brokers understand that markets often tighten gradually before the broader freight economy fully reflects the shift.

“Capacity leaves the market faster than demand returns. That’s why pricing often changes before shipment indexes do.”

Are you watching shipment trends, or are you paying closer attention to available carrier capacity?

What DAT and Cass Say About Rates Versus Shipments

The strongest evidence supporting this market shift comes from two of the industry’s most respected data sources.

According to DAT’s April 2026 report, spot and contract truckload rates reached their highest levels in more than two years. Van, reefer, and flatbed volumes all increased month-over-month, suggesting strengthening freight activity and improving carrier leverage [DAT, 2026].

Meanwhile, the April 2026 Cass Transportation Index tells a more nuanced story.

Cass reported:

| Metric | Year-over-Year Change |

| Shipments | -4.4% |

| Expenditures | +3.5% |

| Truckload Linehaul Index | +5.6% |

At first glance, those numbers appear contradictory.

If shipments are declining, why are expenditures increasing? Why are freight rates rising?

The answer is that pricing is being influenced by capacity conditions rather than a full freight boom.

The industry has spent nearly two years reducing excess capacity. Thousands of small carriers either exited the market or significantly scaled back operations. Fleet growth slowed. Equipment investment slowed. Driver recruitment slowed.

As a result, even moderate freight activity is now exerting greater pressure on available trucks.

For brokers, this changes how customer conversations should be handled.

Instead of focusing exclusively on shipment demand, discussions should include:

- Carrier availability trends

- Lane-specific pricing movement

- Regional capacity constraints

- Equipment availability

- Seasonal volatility risks

The brokers who can explain these dynamics clearly become significantly more valuable to customers than brokers who simply provide rates.

This is where experienced agents separate themselves from transactional competitors.

In our experience, customers are far more likely to accept pricing adjustments when they understand the operational realities driving them.

“The strongest brokers don’t sell freight. They help customers understand the market.”

If a shipper asked why rates are rising despite uneven shipment volumes, could your team explain it confidently?

Why Intermodal Strength Matters Right Now

One of the most overlooked developments in the current freight market news cycle is the growing strength of Intermodal freight.

According to the Association of American Railroads (AAR), intermodal volume increased for a third consecutive month in 2026. April carloads reached their strongest April level since 2019, while the Freight Rail Index climbed to a 16-month high [AAR, 2026].

These developments matter because Intermodal freight often acts as an early signal of broader freight market changes.

When transportation buyers increase their use of intermodal shipping, it usually reflects several important market conditions:

- Supply chains are becoming more active.

- Inventory movement is increasing.

- Transportation planners are seeking cost stability.

- Long-haul freight volumes are improving.

- Capacity management is becoming more strategic.

Many shippers spent the past two years prioritizing flexibility because capacity was abundant and rates were relatively soft.

The current market is beginning to reward planning instead.

| Truckload | Intermodal Shipping |

| Faster transit | Lower cost potential |

| Higher flexibility | Greater capacity consistency |

| Better for short-haul freight | Better for long-haul freight |

| More exposure to spot volatility | More pricing stability |

For brokers, understanding Intermodal freight is becoming increasingly important.

The most effective transportation partners are no longer simply quoting truckload options. They are helping customers evaluate the right mode for the right shipment.

As capacity tightens, mode optimization becomes a competitive advantage.

Companies that understand both truckload and intermodal shipping are often better positioned to control costs and maintain service levels during periods of market transition.

“The next phase of freight competition may be won by brokers who understand mode strategy, not just truckload pricing.”

Are you helping customers evaluate transportation options, or simply quoting truckload rates?

How Enforcement and Carrier Quality Affect Available Capacity

One of the most underappreciated factors affecting capacity currently is enforcement.

Many industry participants still view compliance as an administrative issue. In reality, compliance directly impacts available capacity.

The Commercial Vehicle Safety Alliance (CVSA) reported that during Brake Safety Day in May 2026, 574 vehicles or 14.3% of inspected trucks, were placed out of service due to brake-related violations [CVSA, 2026].

That statistic has significant implications.

Every truck removed from service represents capacity that is no longer available to move freight.

When multiplied across thousands of carriers nationwide, compliance failures can meaningfully reduce the amount of usable capacity in the market.

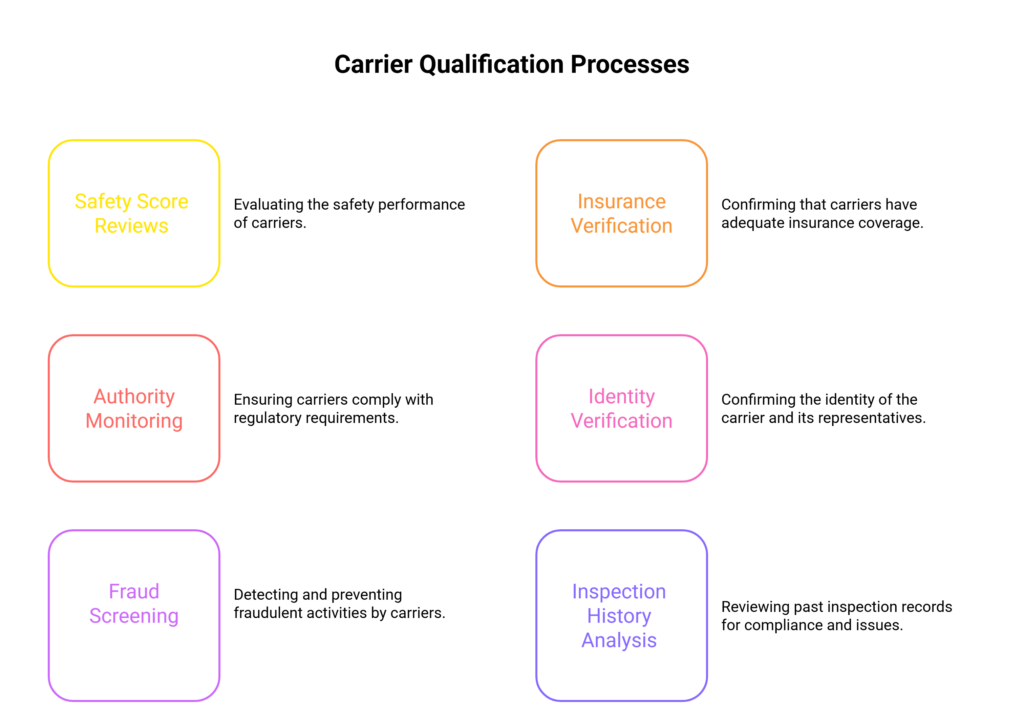

This is particularly important as brokers increase carrier vetting standards.

Currently, carrier qualification processes increasingly include:

- Safety score reviews

- Insurance verification

- Authority monitoring

- Identity verification

- Fraud screening

- Inspection history analysis

The result is that available capacity and qualified capacity are no longer the same thing.

Many carriers technically exist in the marketplace.Fewer meet the operational standards that brokers and shippers increasingly require.

This distinction helps explain why truckload rates can rise even when shipment growth remains uneven.

The market pays for dependable capacity, not theoretical capacity.

“Compliance is no longer a back-office issue. It is becoming a capacity issue.”

How much of the reported capacity would actually qualify for your most important customers?

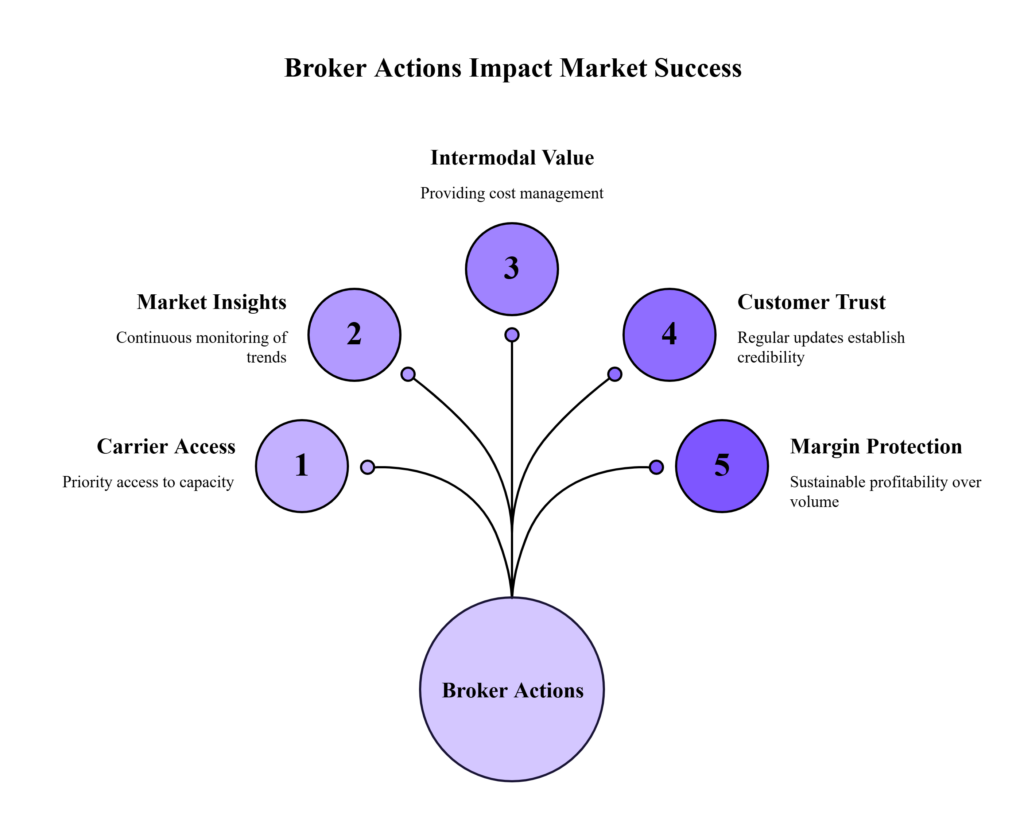

What Experienced Brokers Should Do in the Next 60–90 Days

Markets like this reward preparation. The next few months may create significant opportunities for brokers who position themselves correctly.

Several priorities stand out.

1.Strengthen Carrier Relationships

Quality carriers are becoming more valuable as capacity tightens. Brokers who invest in long-term carrier partnerships often gain access to capacity before competitors do.

2. Improve Market Intelligence

A strong freight market update strategy should include continuous monitoring of:

- Lane-specific rate movement

- Carrier availability trends

- Seasonal freight patterns

- Regional disruptions

- Mode shifts

3. Expand Intermodal Knowledge

Growing Intermodal freight activity suggests that transportation buyers are actively evaluating alternatives to traditional truckload solutions.

Brokers who understand intermodal shipping can provide additional value when customers seek cost management strategies.

4. Increase Customer Communication

Many shippers still believe the market remains unchanged from 2024 or early 2025.

Regular updates on freight market news, capacity conditions, and pricing trends help establish credibility.

5. Protect Margins

Rate pressure often creates a temptation to chase volume.

Experienced brokers know that sustainable profitability matters more than temporary growth.

“The best brokers prepare for market changes before customers start feeling them.”

Wondering what separates agents who grow during market shifts from those who simply react to them? Discover the habits and strategies successful freight agents use to stay ahead.

What Shippers Should Ask Their Brokerage Partners Right Now

Manufacturing continues expanding, but cost pressure remains significant.

According to ISM, April 2026 manufacturing activity remained in expansion territory with a PMI of 52.7. Supplier deliveries registered 60.6 while the prices index reached 84.6, indicating continued pressure on input costs and lead times [ISM, 2026].

For shippers, this environment creates a need for more strategic transportation conversations.

Questions worth asking include:

- What are you seeing in carrier availability?

- How are freight rates changing in our key lanes?

- Where are capacity constraints developing?

- Could Intermodal freight create cost advantages?

- How are you monitoring carrier quality?

- What market risks should we anticipate over the next quarter?

The quality of these answers often reveals the difference between a transportation vendor and a transportation partner.

The most valuable brokerages are increasingly serving as market advisors.

This trend aligns closely with priorities outlined in the USDOT’s 2026 National Freight Strategic Plan, which emphasizes safety, resiliency, efficiency, workforce development, and supply chain reliability [USDOT, 2026].

As freight networks become more complex, shippers need partners capable of translating market conditions into actionable strategies.

“Transportation planning becomes more important during uncertain markets.”

If your brokerage partner disappeared tomorrow, would you lose a vendor or a source of market intelligence?

How SPI Agents and SPI’s Network Respond Differently

Markets like today’s tend to expose the difference between reactive brokers and strategic brokers.

When conditions become uncertain, many market participants focus entirely on load volume.

SPI’s approach places equal emphasis on understanding capacity.

In our experience, brokers who perform well during volatile markets focus on:

- Carrier quality before carrier quantity

- Market intelligence before market assumptions

- Relationship building before transactional growth

- Multi-modal solutions before one-size-fits-all approaches

- Long-term customer trust before short-term wins

As truckload rates continue adjusting and Intermodal freight gains momentum, brokers need more than access to loads.

They need visibility.They need operational discipline. And they need a network capable of adapting as conditions change.

The current freight market update suggests that capacity dynamics, not simply shipment demand, will continue shaping transportation decisions throughout the remainder of the year.

The brokers who recognize that early will likely be the ones creating the most value for customers.

“In uncertain markets, information often becomes more valuable than capacity itself.”

Want to sharpen your market knowledge and make more confident freight decisions in changing conditions? Explore freight broker education and insights designed for experienced transportation professionals.

Frequently Asked Questions (FAQs)

1.Why are truckload rates increasing if shipment demand remains uneven?

Capacity has exited the market faster than demand has recovered. This creates pricing pressure even when shipment growth remains inconsistent across industries [DAT, 2026; Cass, 2026].

2. Why is Intermodal freight gaining momentum in 2026?

Rail and intermodal activity have strengthened due to increasing freight activity, improved inventory movement, and transportation buyers seeking more stable long-haul transportation options [AAR, 2026].

3. What should brokers focus on during tightening market conditions?

Carrier relationships, market intelligence, customer communication, compliance, pricing discipline, and understanding intermodal shipping opportunities should all be priorities.

The Next Freight Shift Is Already Underway

The freight market rarely moves in straight lines, and 2026 is proving that once again.

While shipment demand remains uneven across sectors, the data increasingly points toward a market where capacity is tightening faster than many broad indicators suggest. Rising truckload rates, improving Intermodal freight activity, stronger carrier qualification standards, and ongoing enforcement activity are all contributing to a transportation environment that looks very different from the one brokers and shippers navigated just a year ago.

For brokers, the opportunity lies in understanding these shifts before customers feel their full impact. The most successful brokers over the next several months will not necessarily be the ones moving the most freight. They will be the ones who can interpret market signals, communicate them clearly, and help customers make better decisions in an increasingly complex environment.

For shippers, this is a reminder that transportation planning cannot rely solely on shipment volume data. Capacity quality, mode selection, compliance trends, and market intelligence are becoming just as important as freight demand itself.

The market is not booming. It is not collapsing.It is evolving. And those who understand the difference will be in the strongest position moving forward.

If you already manage a meaningful book of business and want a brokerage platform built for volatile markets, talk with SPI about the agent model.

References

[AAR, 2026] Association of American Railroads. Rail Industry Overview. https://www.aar.org/rail-industry-overview/

[Cass, 2026] Cass Information Systems. April 2026 Transportation Index. https://www.cassinfo.com/freight-audit-payment/cass-transportation-indexes/april-2026

[CVSA, 2026] Commercial Vehicle Safety Alliance. 2026 Brake Safety Day Results. https://cvsa.org/news/2026-bsd-results/

[DAT, 2026] DAT Freight & Analytics. Truckload Freight Rates Hit Two-Year Highs. https://www.dat.com/company/news-events/news-releases/dat-truckload-freight-rates-hit-two-year-highs-as-diesel-costs-surge

[ISM, 2026] Institute for Supply Management. April 2026 Manufacturing PMI Report. https://www.ismworld.org/supply-management-news-and-reports/reports/ism-pmi-reports/pmi/april/

[USDOT, 2026] U.S. Department of Transportation. 2026 National Freight Strategic Plan. https://www.transportation.gov/freight/NFSP