Independent freight brokers often spend 5–20 years building customer relationships, carrier networks, lane expertise, and operational systems. Yet most owners don’t begin planning their exit until burnout, life changes, or market shifts force the decision (Transportation Intermediaries Association [TIA], n.d.).

In our experience working with independent agents and brokerage operators, the difference between a stressful exit and a profitable one comes down to preparation, especially financial documentation, customer diversification, and operational independence from the founder.

Below are the most common and practical exit strategies, explained with real operational considerations.

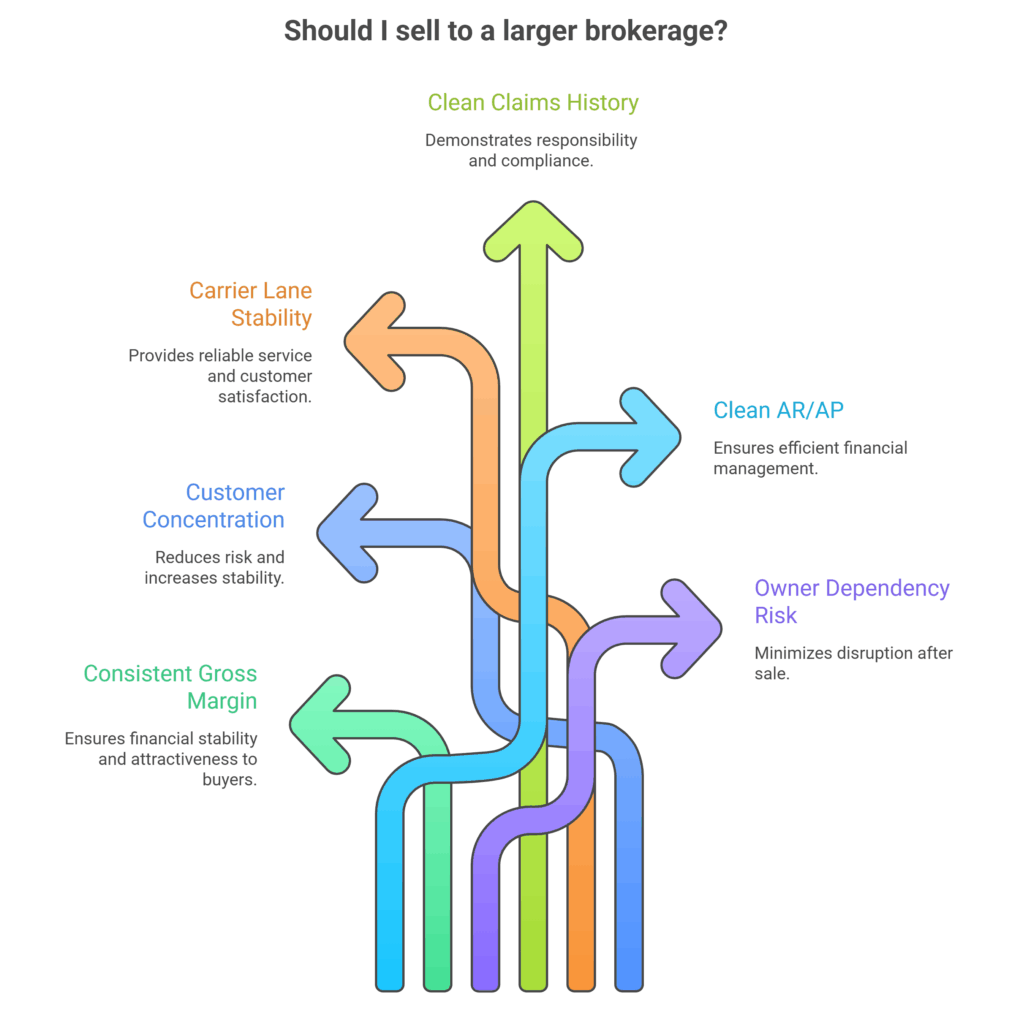

Selling to a Larger Brokerage

Selling to a regional or national brokerage is one of the most common exit paths.

Buyers are typically evaluating:

- 3 years of consistent gross margin

- Customer concentration (no single client >25–30% revenue)

- Carrier lane stability

- Claims history and compliance record

- Clean AR/AP processes

- Owner dependency risk

In acquisitions we’ve observed, valuation multiples for small independent brokerages generally range from 2–4x adjusted EBITDA, depending on revenue consistency and customer retention agreements.

Earn-outs are common. Many deals include:

- 60–80% upfront payment

- 12–24 month revenue retention incentive

- Transition consulting agreement

The smoother your SOPs, CRM records, and TMS documentation, the higher your perceived transferability (FreightWaves, n.d.).

“In our experience, brokers who systemize operations and reduce owner dependency often command stronger multiples because buyers are purchasing transferable infrastructure, not just relationships”

If you stepped away tomorrow, could a buyer run your operation using your documented processes alone?

Passing the Business to Family

Succession planning inside the family can preserve legacy and long-term revenue continuity, but only when structured intentionally (Small Business Administration [SBA], n.d.).

We’ve seen family transitions fail when:

- The successor lacked pricing authority experience

- Carrier negotiations were never delegated

- Financial transparency was unclear

- Emotional expectations replaced formal agreements

Successful transitions typically include:

- 12–24 months of shared authority

- Gradual client introduction meetings

- Documented profit distribution agreements

- Defined leadership roles and compensation

In freight brokerage, real-time decision-making under pressure (missed pickups, payment disputes, emergency reroutes) cannot be learned passively (TIA, n.d.).

“The smoothest family transitions we’ve seen happened when the successor had already handled live freight crises, not just back-office oversight.”

Has your successor managed a high-stakes load failure independently?

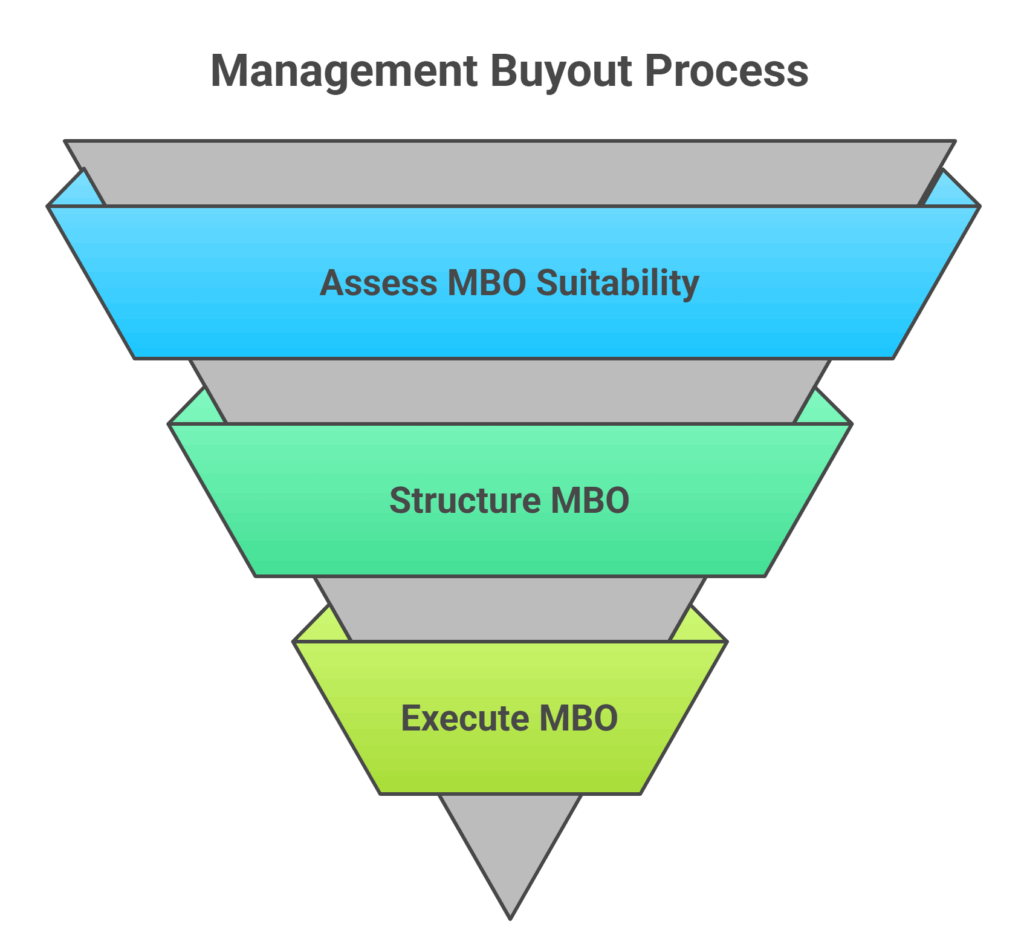

Management Buyout (MBO)

A management buyout allows internal leadership, often a senior agent or operations manager, to purchase the brokerage (FreightWaves, n.d.).

This path works well when:

- Revenue generation is team-based

- Leadership already handles pricing and dispatch

- Financial reporting is clean and transparent

- Client relationships are diversified

Common MBO structures include:

- Seller financing over 3–5 years

- Performance-based payout tied to revenue retention

- Gradual equity transfer

The biggest risk is financing strain if revenue dips during transition.

In our experience, internal buyouts are most successful when the leadership team has already been operating independently for at least 12 months before the transition.

“When managers were already pricing freight, resolving disputes, and handling carrier issues autonomously, post-buyout revenue retention was noticeably stronger.”

Are you preparing your team to take over and continue your brokerage’s success? Discover how structured systems and support can ensure a smooth internal transition with our Freight Brokerage Back Office Support solution.

Merging with Another Brokerage

Mergers allow independent brokers to combine operations and share equity rather than fully exit (SBA, n.d.).

Strategic advantages:

- Expanded freight lanes

- Increased carrier density

- Shared TMS infrastructure

- Reduced overhead duplication

However, mergers require deep operational alignment.

Key integration steps we’ve seen work effectively:

- Unified commission structures

- Shared CRM and financial reporting systems

- Clear authority hierarchy

- Structured 90-day integration roadmap

Without structured integration planning, merged brokerages often struggle with cultural friction or commission disputes.

“The most stable brokerage mergers included written integration timelines covering customer communication, carrier consolidation, and billing system alignment.”

Are you planning to wind down or restructure your brokerage the right way? Explore our Freight Broker Solutions to protect your value and transition with confidence.

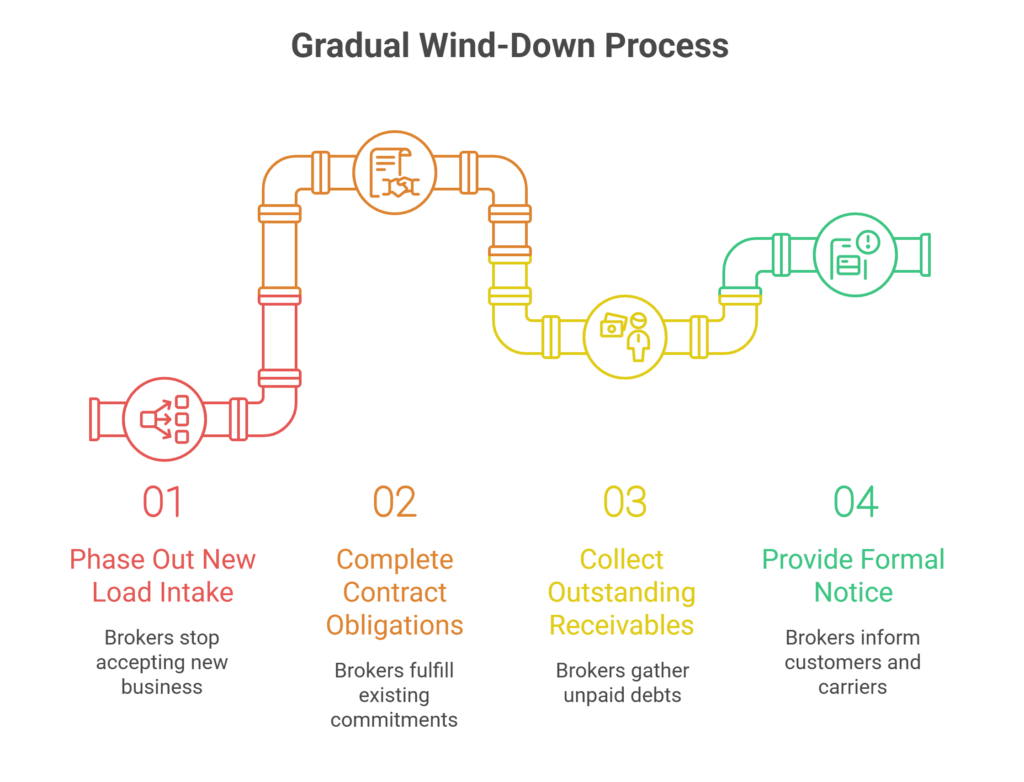

Gradual Wind-Down

Some brokers prefer a controlled exit rather than a sale.

This involves:

- Phasing out new load intake

- Completing contract obligations

- Collecting outstanding receivables

- Providing formal notice to customers and carriers

The key operational risk during wind-down is claims exposure and delayed payments.

From a financial standpoint, wind-downs typically yield less total return than acquisitions, but they provide lower complexity (Federal Motor Carrier Safety Administration [FMCSA], n.d.).

We’ve seen wind-down timelines range from 6–18 months depending on lane commitments.

“When wind-down plans were structured over 9–12 months with clear receivable tracking, brokers avoided legal and compliance complications.”

How long would it realistically take to clear all receivables and carrier obligations in your business?

Selling the Customer Book Only

In this model, brokers sell their active accounts to another brokerage without transferring the entire business entity (FreightWaves, n.d.).

Compensation is often structured as:

- Percentage of retained revenue over 6–18 months

- Tiered payout based on customer retention

- Introductory transition period

This method works best when:

- Customer contracts are stable

- Lane history is documented

- Pricing agreements are transparent

However, customer loyalty risk is higher if relationships are tied personally to the owner.

“Customer-book exits are strongest when contracts, rate histories, and billing records are thoroughly documented, reducing transition friction.”

Are your client relationships attached to your brokerage brand, or your personal relationships?

Real-World Case Study: Strategic Acquisition Exit

An independent freight broker with seven years in operation decided to pursue a strategic acquisition after reaching consistent annual revenue of $8.2 million with an 18% average gross margin. The brokerage maintained 42 active customers, but revenue concentration presented a risk: one client accounted for 34% of total annual revenue. Operationally, the owner was heavily involved in pricing, personally handling nearly 80% of rate negotiations and margin approvals. Invoicing was largely manual, and there were no formalized standard operating procedures for carrier onboarding or claims handling.

Recognizing that buyer valuation would be impacted by owner dependency and customer concentration risk, the broker initiated an 18-month preparation strategy prior to formally entering acquisition discussions. During that period, the brokerage intentionally diversified revenue streams, reducing the largest customer’s share of total revenue from 34% to 22%. Pricing authority was gradually transferred to a senior agent, allowing the owner’s direct operational involvement to decrease to approximately 40% of daily execution. A Transportation Management System (TMS) was implemented to centralize reporting, margin tracking, and carrier performance data. Carrier onboarding procedures were standardized, and minimum margin thresholds were formally documented to ensure consistency across lanes.

By the time acquisition conversations formally began, annual revenue had grown to $9.1 million and gross margin had improved to 19.4% due to standardized pricing discipline. Financial reporting was cleaner, accounts receivable cycles were more predictable, and operational processes were transferable rather than relationship-dependent. These improvements materially changed buyer perception.

The brokerage ultimately sold to a mid-sized regional brokerage at a 3.5x adjusted EBITDA multiple. The deal structure included 70% upfront cash with an 18-month earn-out tied to achieving 90% revenue retention. Due to structured client transition planning and documented operating systems, 94% client retention was achieved during the earn-out period. Preparation over the 18 months prior to sale was estimated to have increased enterprise value by approximately 25–30% compared to an immediate sale under the original operational structure.

“In our experience, the largest valuation increases come not from revenue growth alone, but from reducing owner dependency and documenting systems that allow the business to operate independently of the founder.”

If you began preparing your brokerage for sale 12–18 months in advance, which operational weaknesses would most affect your valuation?

Protect Your Brokerage’s Value

Exit strategy is not just about leaving, it’s about protecting the value you’ve built. Whether through acquisition, succession, buyout, merger, or wind-down, the strongest exits are planned early, documented clearly, and executed with operational transparency.

Brokers who prepare financials, formalize systems, and reduce owner-dependency consistently experience smoother transitions and stronger financial outcomes.

Ready to position your brokerage for a smooth and profitable exit, whenever the time comes? Contact us to strengthen your operations and protect your long-term value.

Frequently Asked Questions (FAQs)

1. How is the value of an independent freight brokerage determined?

The value of an independent freight brokerage is typically based on adjusted EBITDA, revenue consistency, customer concentration risk, and operational transferability. Most small to mid-sized brokerages sell within a 2x–4x adjusted EBITDA multiple range, depending on margin stability and how dependent the business is on the owner. Clean financial reporting, diversified customers, and documented processes significantly improve valuation outcomes.

2. How long does it take to prepare a freight brokerage for sale?

In most cases, brokers should allow 12–24 months of preparation before actively pursuing a sale. This timeline allows for revenue diversification, operational systemization, financial cleanup, and leadership delegation. Rushed exits often result in lower multiples because buyers perceive higher risk.

3. What is the biggest mistake freight brokers make when planning an exit?

The most common mistake is waiting too long to prepare. Many owners delay exit planning until burnout or market downturns force action. At that point, customer concentration, undocumented processes, and owner dependency reduce negotiating leverage. Early preparation, especially reducing reliance on the founder, consistently leads to smoother transitions and stronger financial outcomes.

References

Federal Motor Carrier Safety Administration. (n.d.). Regulations and compliance guidance. Retrieved from https://www.fmcsa.dot.gov

FreightWaves. (n.d.). Freight brokerage mergers and acquisitions insights. Retrieved from https://www.freightwaves.com

Small Business Administration. (n.d.). Business succession planning guidance. Retrieved from https://www.sba.gov

Transportation Intermediaries Association. (n.d.). Freight broker industry resources. Retrieved from https://www.tianet.org